Impact of Covid19 on Farming Industry in Australia

August 14, 2020

With some significant exceptions, rapid and comprehensive action has meant that COVID-19 has not had a severe impact on most of Australia’s agricultural industries. This has limited the amount of adaptation required.

As the COVID-19 pandemic spreads, so will the impacts on Australia’s agriculture, forestry, and fisheries sectors. Initially, the impact was due to slowing demand in China, however, the subsequent global spread of the virus is now impacting on global markets, making the short-term outlook for Australian agriculture increasingly uncertain.

The first impact of COVID-19 on Australia’s agricultural value chains was from panic buying. As expected, panic buying at the start of the pandemic proved to be a short-term shift in the timing of purchasing. Retail purchasing has since fallen below seasonal norms as household stockpiles have been consumed.

The next most significant impact of COVID-19 on agricultural value chains came from the measures introduced to slow the spread of the disease. Specialist horticultural, wine, and other businesses tailoring production toward restaurants and the food services industries have been significantly impacted. The lockdowns shifted consumption from higher-value products sold in restaurants and food services toward lower-value staples consumed at home. Industries like horticulture and wine are also labor-intensive, and so have been most affected by the additional costs of introducing social distancing. In broadacre agriculture, the wool industry has also been affected by social distancing for shearers, while the meat processing and live animal export industries have been affected by a small number of abattoir and shipping outbreaks.

The demand for Australian exports of food staples has remained steady. The demand for food staples is likely to be less affected by COVID-19 related falls in incomes

Higher value exports have been impacted. Lockdowns in Australia’s export markets have shifted consumption from products destined for restaurants and the food services industries to products purchased in supermarkets and consumed at home. Seafood has been the most affected industry, along with wine, horticulture, and some higher value livestock and dairy products. The Australian Government has responded with financial assistance to facilitate airfreight to alternative markets.

Global lockdowns that abruptly curtailed retail clothing sales significantly impacted the demand for Australia’s wool exports. Wool exports were also affected by measures to contain the spread of COVID-19 in the yarn, textile and clothing manufacturing industries in importing nations such as China. Wool has also been affected by low oil and synthetic fibre prices and an income-related fall in demand for high-value clothing. Australia’s cotton industry would also have been significantly affected had the 2019–20 crop not been dramatically reduced by drought.

However, in general, industry adaptation both in Australia and abroad has reduced the impact of COVID-19 on Australia’s agricultural industries (see box). For example, the producers of high-value foods and wine have dramatically expanded online pathways for marketing directly to households. Labour-intensive industries have adapted to social distancing requirements to continue operations, albeit with additional costs and reduced productivity. Lockdown effects on agricultural and veterinary supply chains to Australia proved short term, with minimal additional disruptions to supply beyond the effects of drought.

Adapting to COVID-19

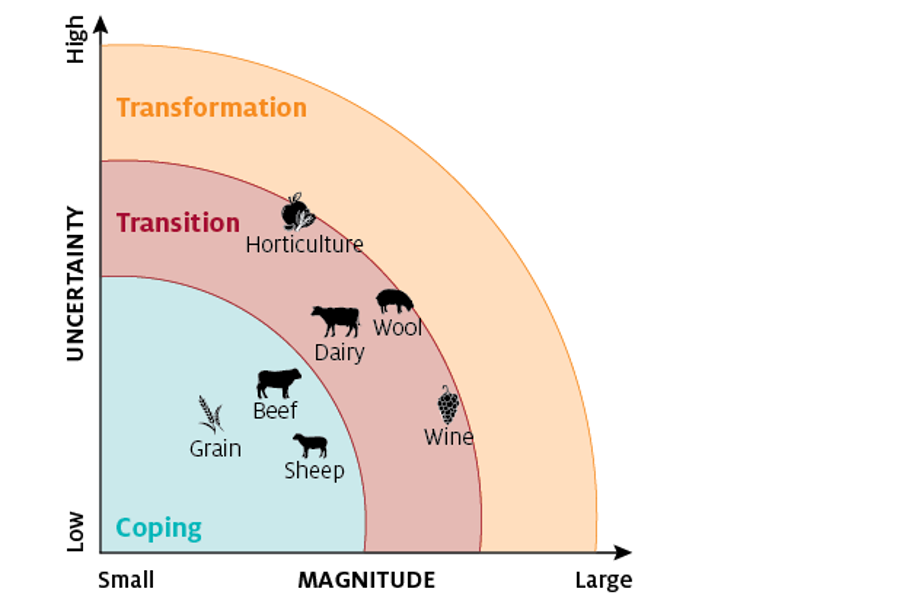

The degree of adaptation required to cope with COVID-19 varies from industry to industry based on the magnitude of its impacts and the degree to which these are predictable. Pelling (2010) described 3 levels of adaptation that may be required for industries to be resilient to the impacts of change.

For impacts that are reasonably predictable or small, only minor adaptation may be needed to cope with them.

Impacts that are less predictable or more significant may need adaptation that pushes existing ways of doing things close to their limits (transitional adaptation).

Impacts that are deeply uncertain or overwhelming may require entirely new ways of doing things (transformational adaptation).

Effective containment strategies have meant that most of the adaptation taking place to COVID-19 in Australian agriculture has been relatively minor ‘coping’—well within the existing limits of current businesses and industries. Because containment has been effective, Australia’s agricultural businesses have mostly had to adapt to the effects of containment measures rather than the effects of the virus itself.

Adaptation by Australia’s agricultural industries to COVID-19

Get the full report here:

https://www.agriculture.gov.au/abares/research-topics/agricultural-outlook/agriculture-overview

Article reproduced from original source:

https://www.agriculture.gov.au/abares/research-topics/agricultural-outlook/agriculture-overview